Another Monday Message Board. Post comments on any topic. Civil discussion and no coarse language please. Side discussions and idees fixes to the sandpits, please.

Announcements from major employers, including Amazon and Tabcorp, that workers will be required to return to the office five days a week have a familiar ring. There has been a steady flow of such directives. The Commonwealth Bank CEO, Matt Comyn, attracted a lot of attention with an announcement that workers would be required to attend the office for a minimum of 50% of the time, while the NSW public service was recently asked to return to the office at least three days a week.

But, like new year resolutions, these announcements are honoured more in the breach than the observance. The rate of remote work has barely changed since lockdowns ended three years ago. And many loudly trumpeted announcements have been quietly withdrawn. The CBA website has returned to a statement that attracts potential hires with the promise, “Our goal is to ensure the majority of our roles can be flexible so that our people can work where and how they choose.”

The minority of corporations that have managed to enforce full-time office attendance fall into two main categories. First, there are those, like Goldman Sachs, that are profitable enough to pay salaries that more than offset the cost and inconvenience of commuting to work, whether or not they gain extra productivity as a result. Second, there are companies like Grindr and Twitter (now X) that are looking for massive staff reductions and don’t care much whether the staff they lose are good or bad.

Typically, as in these two cases, such companies are engaged in the process Cory Doctorow has christened enshittification, changing the rules on their customers in an effort to squeeze as much as possible out of them before time runs out.

We might be tempted to dismiss these as isolated cases. But a recent KPMG survey found that 83% of CEOs expected a full return to the office within three years. Such a finding raises serious questions, not so much about remote work but about whether CEOs deserve the power they currently hold and the pay they currently receive.

Another Monday Message Board. Post comments on any topic. Civil discussion and no coarse language please. Side discussions and idees fixes to the sandpits, please.

Like most academics these days, I spend a lot of time filling in online forms. Mostly, this is just an annoyance but occasionally I get something out of it. A recent survey in which the higher-ups tried to get an idea of how the workforce was feeling, asked the question “Do you think of the University as We or They?”.

Another Monday Message Board. Post comments on any topic. Civil discussion and no coarse language please. Side discussions and idees fixes to the sandpits, please.

Another Monday Message Board. Post comments on any topic. Civil discussion and no coarse language please. Side discussions and idees fixes to the sandpits, please.

In today’s AFR. It’s paywalled and I don’t have access (I’ve been promised a PDF) so here’s what I submitted, which may not be final.

Six months ago, Federal Treasurer Jim Chalmers was planning legislation to remove his own power (never used, but always available until now) to over-ride decisions of the Reserve Bank. Now, he has not only decided to retain this power, but has openly criticised the Bank’s interest rate decisions as “smashing the economy”.

It’s easy enough to understand Chalmer’s criticism in terms of the political interests of a government seeking to survive and retain power. The government is focused, to the point of obsession, on the “cost of living”, a nebulous term that can best be interpreted as “the reduced purchasing power of household disposable income”.

This study showing that US academic faculty members are 25 times more likely than Americans in general to have a parent with a PhD or Masters degree has attracted a lot of attention, and comments suggesting that this is unusual and unsatisfactory. But is it? For various reasons, I’ve interacted quite a bit with farmers, and most of them come from farm families. And historically it was very much the norm for men to follow their fathers’ trade and for women to follow their mothers in working at home.

So, I decided to look for some statistical evidence. I used Kagi’s AI Search, which, unlike lots of AI products is very useful, producing a report with links to (usually reliable) sources. That took me to a report by the Richmond Federal Reserve which had a table from a paper about political dynasties.

The latest massive $1.1bn profit reported by Coles will doubtless produce a new round of hand-wringing about the “cost of living”. Governments will produce initiatives aimed at capping or reducing prices. Pundits will use a variety of measures to argue as to whether such measures are inflationary. Then there will be debates about whether splitting up Coles and Woolworths into smaller chains would enhance competition. And the Reserve Bank will be encouraged to push even harder to return inflation to its target range.

But these responses, focused on the cost of goods, miss the point. Coles and Woolworths have increased their margins, yes – but prices for groceries have increased broadly in line with other goods. The real driver of supermarket profits is their ability to drive down the prices they pay to suppliers.

But the input that matters here is labour and it is here that the supermarkets are making big gains at the expense of their workers. Across the board, wages have failed to keep pace with prices over the last five years or more.

At least for the supermarkets, this won’t change any time soon.

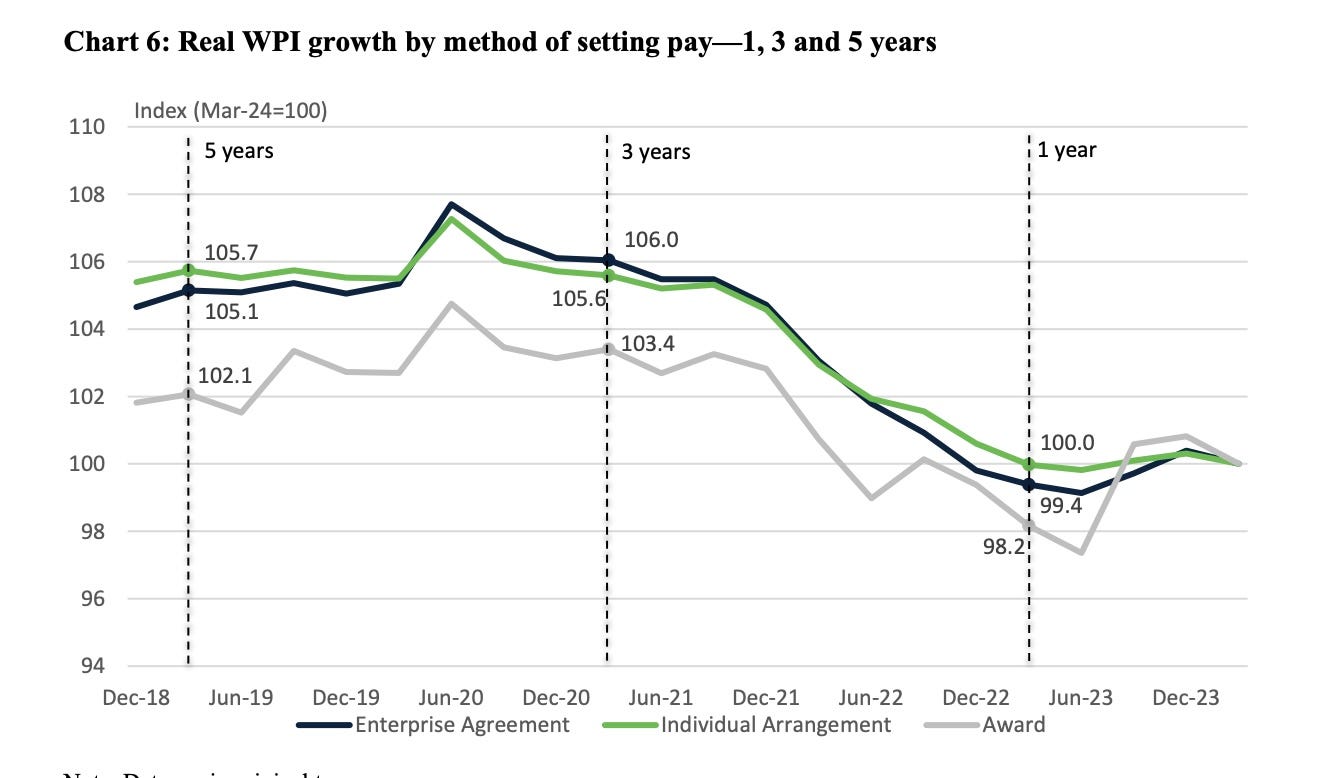

Yet again, the FWC declined to do anything about the fall in real wages that has taken place since the arrival of the pandemic, compounding a long period of stagnation before that. As it noted: “Despite the increase of 5.75 per cent to modern award minimum wage rates in the AWR 2023 decision, the position remains that real wages for modern award-reliant employees are lower than they were five years ago.”

Real WPI growth by method of setting pay – 1, 3 and 5 years. Photograph: FairWork Commission

There is no cost of living crisis for those whose income derives from profits. Those at the top end of town have seen their incomes soar. But even more modestly wealthy recipients of capital income are doing well, a fact reflected in their spending patterns.

To be sure, old people, such as self-funded retirees, are more likely to be receiving capital income and less likely to be reliant on wages to pay mortgage interest. But this is by no means universal. Plenty of baby boomers are still in the workforce, while some of our most prominent property owners (such as Tim “avocado toast” Gurner) are much younger. Focusing on age merely confuses a debate that is already complicated enough.

The policies of the Reserve Bank make matters even more thorny. The problems here start with a dogmatic adherence to a 2% to 3% inflation target. The rationale for inflation targeting is thin, and the choice of target range is entirely arbitrary, arising from an ad hoc decision by a right-wing New Zealand finance minister in the early 1990s, one which was followed by a long period of economic decline in that country.

The dangers of using high interest rates to achieve rapid reductions in inflation, evident from the “credit squeezes” of the 1970s and 1980s, are now becoming apparent, as the drive to reduce inflation is reflected in a push to squeeze demand and prevent any recovery in real wages.

There is little hope that all of this will change any time soon. The concept of “cost of living” is simple and intuitive, even if it is highly misleading. What really matters is the purchasing power of people’s disposable incomes. But that’s a bit too hard for our political class to think about, let alone explain to the public.

Another Monday Message Board. Post comments on any topic. Civil discussion and no coarse language please. Side discussions and idees fixes to the sandpits, please.