My latest piece in The Conversation is one of six looking at changes in various aspects of Australian life since the turn of the century. Most of it is a recounting of the history, but I have a few things to say at the end about the information economy

The most striking feature of the Australian economy in the 21st century has been the exceptionally long period of fairly steady, though not rapid, economic growth.

The deep recession of 1989–91, and the painfully slow recovery that followed, led most observers to assume another recession was inevitable sooner or later.

And nearly everywhere in the developed world, the Global Financial Crisis of 2007–08 did lead to recessions comparable in length and severity to the Great Depression of the 1930s.

Through a combination of good luck and good management, Australia avoided recession, at least as measured by the commonly used criterion of two successive quarters of negative GDP growth.

Recessions cause unemployment to rise in the short run. Even after recessions end, the economy often remains on a permanently lower growth path.

Good management – and good luck

The crucial example of good management was the use of expansionary fiscal policy in response to both the financial crisis and the COVID pandemic. Governments supported households with cash payments as well as increasing their own spending.

The most important piece of good luck was the rise of China and its appetite for Australian mineral exports, most notably iron ore.

This demand removed the concerns about trade deficits that had driven policy in the 1990s, and has continued to provide an important source of export income. Mining is also an important source of government revenue, though this is often overstated.

Still more fortunately, the Chinese response to the Global Financial Crisis, like that in Australia, was one of massive fiscal stimulus. The result was that both domestic demand and export demand were sustained through the crisis.

The shift to an information economy

The other big change, shared with other developed countries, has been the replacement of the 20th century industrial economy with an economy dominated by information and information-intensive services.

The change in the industrial makeup of the economy can be seen in occupational data.

In the 20th century, professional and managerial workers were a rarefied elite. Now they are the largest single occupational group at nearly 40% of all workers. Clerical, sales and other service workers account for 33% and manual workers (trades, labourers, drivers and so on) for only 28%.

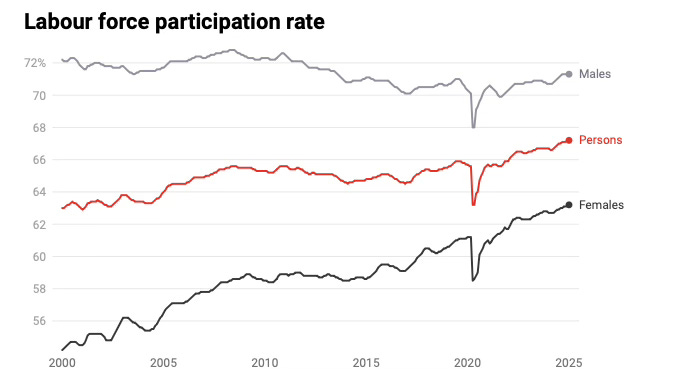

The results are evident in the labour market. First, the decline in the relative share of the male-dominated manual occupations has been reflected in a gradual convergence in the labour force participation rates of men (declining) and women (increasing).

Suddenly, work from home was possible

Much more striking than this gradual trend was the (literally) overnight shift to remote work that took place with the arrival of COVID lockdowns.

Despite the absence of any preparation, it turned out the great majority of information work could be done anywhere workers could find a desk and an internet connection.

The result was a massive benefit to workers. They were freed from their daily commute, which has been estimated as equivalent to an 8–10% increase in wages, and better able to juggle work and family commitments.

Despite strenuous efforts by managers, remote or hybrid work has remained common among information workers.

CEOs regularly demand a return to full-time office work. But few if any have been prepared to pay the wage premium that would be required to retain their most valuable (and mobile) employees without the flexibility of hybrid or remote work.

The employment miracle

The confluence of all these trends has produced an outcome that seemed unimaginable in the year 2000: a sustained period of near-full employment. That is defined by a situation in which almost anyone who wants a job can get one.

The unemployment rate has dropped from 6.8% in 2000 to around 4%. While this is higher than in the post-war boom of the 1950s and 1960s, this is probably inevitable given the greater diversity of both the workforce and the range of jobs available.

Matching workers to jobs was relatively easy in an industrial economy where large factories employed thousands of workers. It’s much harder in an information economy where job categories include “Instagram influencer” and “search engine optimiser”.

As we progress through 2025, it is possible all this may change rapidly, for better or for worse.

The chaos injected into the global economy by the Trump Administration will radically reshape patterns of trade.

Meanwhile the rise of artificial intelligence holds out the promise of greatly increased productivity – but also the threat of massive job destruction. Economists, at least, will be busy for quite a while to come.

It will surprise nobody, I suppose, that I am far less sanguine than most about the overall future prospects of our society, nation and globe.

Firstly though, I do agree there have been good outcomes and good developments. Avoiding recessions is good. Correct and effective use of expansionary fiscal policy when it is necessary is good. Keeping involuntary unemployment low or as low as possible is good. Convergence in the (voluntary) labour force participation rates of men and women is good. Next, we need to see more and more rapid convergence in their pay rates for equal work. The shift to remote (information) work is good. All these things are good and beneficial.

The freeing of people from back-breaking physical labour is also good, especially in places like Australia where heat, humidity, UV and inclement weather extremes are on the rise. The resulting outcomes in wet bulb temperature and in uncomfortable to unsafe outdoor working conditions are also on an inexorable, albeit cyclical, rising trajectory.

This gets me to my point. Things overall are not getting better. They are getting worse despite the fact that there have been some good outcomes and good developments. Our national health crisis deepens as health is chronically under-funded. Also, people are now chronically and serially infected with more and more serious infectious diseases, including Covid-19, many of which our government and medical establishment perversely refuse to minimise with sufficient public health and disease prevention measures.

Our housing crisis deepens. Our homelessness crisis intensifies. Social exclusion worsens. Our crime rates continue to rise. Our housing, infrastructure, transport and communication stock and associated hardware continue to deteriorate and the bulk of new stuff built is sub-standard and rapidly shows signs of premature deterioration and breakdown, especially in the face of rising climate crisis challenges.

Frankly, I consider that much of the business-economic, political and managerial professions’ obsession with non-real indicators, rather than with real indicators, is a central part of our misinformation and disinformation problem. Only real stuff matters. Non-real, notional measures like money, finance, GDP etc. are next to worthless in gauging the state of real systems. Indeed, used the way they are today in public discourse, they are probably worse than useless.

For example, even counting most “social influencers”, most of the media, most advertisers in the advertising industry and many managers as even doing useful work is almost certainly spurious. The bulk of their “work” is a negative drain on resources and creates negative results and negative externalities which far outweigh any positive outcomes of their work.

Indiscriminately counting “information” in bulk as productive and valuable is a most invalid procedure. The information revolution, which did have many positive outcomes, has unfortunately also unleashed industrial quantities (or is the term now tecno-quantities?) of misinformation and disinformation which have played a central role in destroying our response to Covid-19 and destroying democracy in the United States, to name just two issues. These compounding travesties alone have done incalculable to people, societies, nations, climate and environment. Then there’s the crypto-currencies travesty. I could go on.

I would advocate only mentioning real stuff, counts and measures of real stuff, and ways and methods of obtaining enough valid data on real stuff and publicising it. And then only discuss and advocate based on real measures. Where is our national life expectancy graph heading? Where is our homelessness graph heading? Where is our housing availability graph heading? How many people have Long Covid and what types? Which diseases on the rise? How many acres of various land uses and terrestrial nature reserves are we losing to sea level rise per annum? What is the rise in wet bulb temperatures doing to human and worker health, locality by locality? I could go on.

We need biophysically conditioned economics with the fullest possible emphasis on the physical and the bio. Real stuff as I call it. We do not need economics as it is currently practiced and spruiked in public discourse (as distinct from academic discourse which can be more nuanced… maybe). In public discourse, economics is mere economism centred around the fetishistic obsession with spurious, aggregate, nominal measures in the non-scientific dimension of the numeraire. I don’t think feeding this beast (public discourse economism) gets us anywhere. A more radical attempt at re-educating the public is necessary.

Footnote: Information is real too. It exists as real patterns instantiated in real media: patterns which can influence other patterns and indeed generate the growth and propagation of further and new patterns and well as generate growth simpliciter (with the input of energy and/or further mass into the growing system). This usage of “growth” I must say is quite separate in quality and intention from the growth fetishism of endless growth economics.