In a recent post, I pointed out that long-term (30 year) real interest rates on safe (AAA) bonds had fallen to zero, and suggested that this meant the end of capitalism, at least in the sense that the term was understood in classical economics. On the other hand, stock markets have been doing very well. So what is going on? This is a complicated story and I’m still working it out,

An important starting point is the fact that the most profitable companies, particularly tech companies, don’t have all that much in the way of capital assets compared to their market value. What they have is monopoly power, which has been increasing steadily over time. That benefits those who already own and control these firms, but it does not provide new investment opportunities.

I’ll start by looking at price-to-book ratios. Alphabet, which owns Google has a market value five times the book value of its assets https://www.macrotrends.net/stocks/charts/GOOG/alphabet/price-book The ratio is 15 for Microsoft and 21 for Apple. By contrast, for General Motors, the classic 20th century corporation, it’s just under 1.

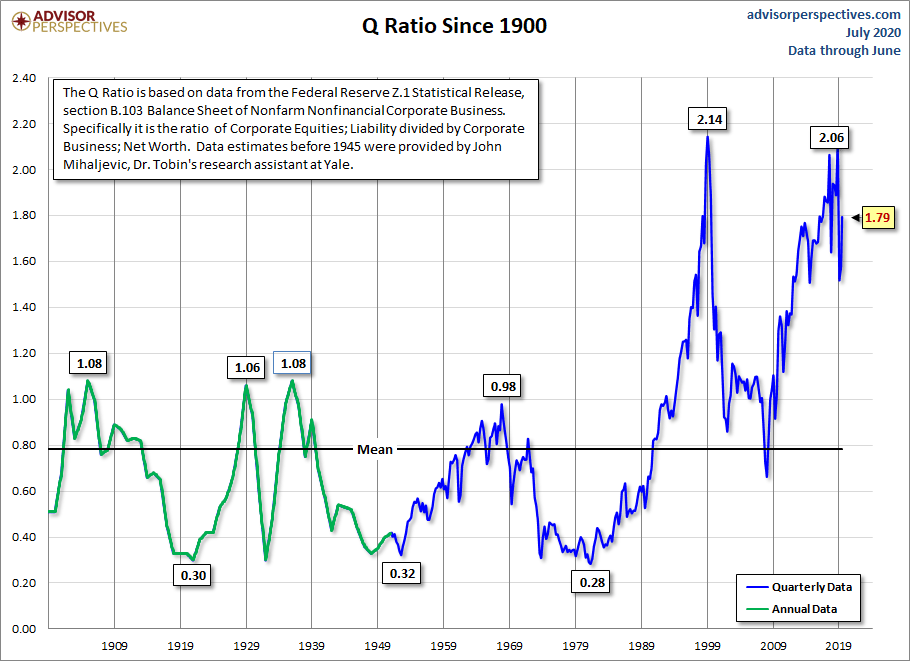

For the corporate sector as a whole, the comparable measure is Tobin’s q ratio, which has been trending upwards since the late 1970s and is now near the all-time high reached during the dotcom bubble.

The value of companies like Apple, Google and Microsoft is made up primarily of “intangibles”. That term can cover all sorts of things, and is often taken to refer to some special aspect of the firm in question, such as accumulated R&D, tacit knowledge or ‘goodwill’ associated with brands.

R&D is at most a small part of the story. The leading tech companies spend $10 – 20 billion a year each on R&D https://spendmenot.com/top-rd-spenders/, a tiny fraction of market valuations of $1 trillion or more. And feelings towards most of these companies are the opposite of goodwill – more like resentful dependence in most cases.

A simpler explanation is that the main intangible asset held by these companies is monopoly power, arising from network effects, intellectual property, control over natural resources and good old-fashioned predatory conduct.

In this context, the crucial point about intangibles isn’t that they aren’t physical, it’s that they can’t be reproduced by anyone else. No one can sell a Windows or Apple operating system, even if they were willing to invest the effort required to reverse-engineer it. While there are competitors for the Google’s search engine (I recommend DuckDuckGo), there are huge barriers to entry, notably including the fact that the product is ‘free’ or rather supported by advertising for which all consumers pay whether they use Google or not.

There’s a complicated relationship here between the rise of monopoly and the development of the information economy in which the top tech firms operate. Information is the ultimate ‘non-rival’ good. Once generated by one person it can be shared with anyone else without diminishing in value. As the cost of communication has fallen, it’s become possible for everyone in the world to gain access to new information at essentially zero cost.

What this means is that there is very little relationship between the value of information and the ability of corporations to capture value from it. The protocols and languages that make the Internet possible are a public good, created by collaborative effort and made freely available. The information on the Internet is generated by households, business and governments using these protocols. Without these public goods, Google would be worthless. But because advertising can be attached to search results, ownership of a search engine is immensely profitable.

In turn, this means that traditional ideas about capital and investment are largely irrelevant in the information economy. More on this soon, I hope.

John I think a few details that you could consider in this story are a kind of sunk cost problem, and also the quality of the product. In terms of the former, it’s almost impossible for a new operating system to enter the market because before anyone will use it widely it needs to be able to support major software products. By this I don’t just mean office, but also all the other specialist software people use (although you shouldn’t overlook office). For me this means latex, Stata, some kind of GIS software, and a reference management software. For a radiologist this means an incredibly complex piece of image processing and storage software that has a very expensive license and makes a very expensive piece of equipment a brick if you don’t have it. I would love to see an alternative OS to Mac OS or Windows but I can’t use it until the other software works on it, and companies like Stata are not going to burn huge amounts of development time on porting their software to a small niche OS. This feeds into MS’s monopoly on office software – I can’t use a new OS that doesn’t support word because I need to share documents with colleagues nationally and internationally who are used to word. This interdependence problem (to coin an idea popularized by Farrell) prevents e.g. China from developing an alternative to windows so they can sell entirely native-made computers, because it kills their international competition.

The other problem here is the quality of the product. Anyone who has tried to use baidu for search will understand quickly that google is vastly superior. You just don’t want to use anything else if you want your search to work. This is a big barrier to entry for competitors, and it needs to be taken into account.

Finally, for social media monopoly is essential. The entire point of Facebook is that everyone is connected. If there are 10 different social networks they’re all useless. This is part of why Wechat and the tencent universe is so good – because everyone is on it. Competition doesn’t work for a product that depends on richness and coverage of a network. This is a weird kind of monopoly but I don’t think it’s necessarily bad in the sense that monopolies on physical products can be, and I can’t see a way around it for a social media product.

These three problems are big intangibles, and I don’t think they necessarily are reflected in things like amount spent on R&D, or numbers of patents held, or anything like that.

faustusnotes, I think a large part of what you’re referring to is covered by the reference John Quiggin has made to ‘network effects’ (if I understand correctly what economists mean by ‘network effects’).

I’m quite interested in reading more analysis on this and many of the recent topics. I’m also interested on where those R&D costs come from as both R&D/IP/AI/whatever are used/abused but many of these “Intangible” platform providers for tax deductions often claimed from costs incurred in a foreign country.

faustusnotes, while I agree with your point about the importance of network effects and incumbency in keeping people stuck on proprietary operating systems, you picked some really bad examples to support those points.

LaTeX and Stata both run very nicely on “minority” operating systems such as Linux.

Furthermore, LaTeX is free software, and it just so happens that there are excellent free software reference management systems (e.g. Zotero) that are cross-platform and/or web-based.

Finally, Stata like all proprietary stats software is currently getting its arse handed to it by R (free software).

So it’s not all doom and gloom for those of us who support software freedom.

Nope, I’m just not getting it. Capitalism consists of more that rentiers and tech behemoths. Just because they’re not in the news does not mean they don’t exist or don’t matter. As we’ve learned over the last couple of months there are companies in Australia that make and sell toilet paper. Presumably they make a profit by doing so. We couldn’t live without them unlike Facebook…That’s still capitalism and I don’t see it ending any time soon.

Malcolm, I agree my examples aren’t great because there’s a lot more proprietary stuff out there that is more focused than Stata. But regarding e.g. Stata runs on Linux, the reason it runs on Linux is that it used to be used on Unix back when Unix was not niche, and was a viable competitor to Windows (I started my scientific career on SparcStations which were vastly superior to windows and MacOS at that time). But if someone set up a new OS now – e.g. chromeOS or whatever it’s called – I find it unlikely Stata would port to that system. They just wouldn’t waste their time and money. Linux has become a niche software platform but the reason Stata works on it (and indeed the reason it works on Mac OS) is that it was developed for Unix when Unix wasn’t niche. Not because Stata charitably ported their software across to those OSs. So even this bad example still shows the power of dependency.

[I think this power of dependency is also part of the reason Linux remains a solid competitor in servers, even though Windows and Mac both improved their server functionality in the past 10 years – because so many servers have been set up that way, and shifting across is more burden than just continuing with Linux].

Also, I don’t want to turn this into a debate about OS and software but Stata is absolutely not getting its arse handed to it by R – R is extremely unreliable and dubious software with a lot of problems, and although it can be very useful for some stuff, it can’t be trusted (my blog has a billion examples of the problems of using R). Stata and SAS are still the industry standard in health science, and it’s extremely hard for many people to move to a new OS while they can’t port their software with them.

faustusnotes, just a datapoint for you. I’m a statistician, I work in health and we are basically a SAS shop. In fact, I’ve been using SAS for about 10 years, R for about 20 and have dabbled in Stata (was used in my Masters).

Sure R suffers from its ‘let a thousand flowers bloom’ nature. But I can tell you that SAS for all its strengths is (slowly) on the way out. Universities don’t teach it anymore and all the new graduates know R and don’t want to use anything else. And despite the conservatism of my workplace, we are building new systems to let them do that.

this means that traditional ideas about capital and investment are largely irrelevant in the information economy

The other traditional idea that’s become irrelevant is the idea of taxing companies, specifically but not limited to the “information economy” ones.

I will note that Shimshon Bichler and Jonathan Nitzan write about this very topic quite extensively in their book “Capital as Power”, first published 2009.

Click to access 20090522_nb_casp_full_indexed.pdf

Clearly Marxists, Veblenians and Capital as Power (CasP) theorists have been writing about this issue for quite some time. Are more orthodox economists just discovering this issue or has it been in the orthodox literature for some time? This is a leading question of course but I don’t think it’s an impertinent question.

I recommend all economists should read it. Clearly you can skip or skim anything that adds nothing to your current knowledge and/or beliefs. But there might be some new potentially intriguing insights, whether or not you are finally convinced by the arguments.

“He who knows only his own side of the case knows little of that. His reasons may be good, and no one may have been able to refute them. But if he is equally unable to refute the reasons on the opposite side, if he does not so much as know what they are, he has no ground for preferring either opinion… Nor is it enough that he should hear the opinions of adversaries from his own teachers, presented as they state them, and accompanied by what they offer as refutations. He must be able to hear them from persons who actually believe them…he must know them in their most plausible and persuasive form.” – John Stuart Mill.

Malcolm, so am I. I have used R a long time, but I prefer Stata for important tasks because I trust it not to fail. But even R is a good example of the dependency problem – as far as I know there is no native version of R for Chrome, iOS or Android. I also stopped using SAS about 10 years ago but based on a cost-benefit calculation and because back then it was slow. I think it’s still heavily used in many environments though (e.g. last time I checked NSW Health’s HOIST system is still built on SAS) and there’s a huge cost to shifting over. Just for me personally, without any institutional issues on top, I have a huge personal library of R code and Stata code, and it would be crazy to try and switch to SAS or SPSS now. This dependency problem exists across the IT world and it doesn’t necessarily have any connection to which software is better, just the software that was used.

I think as the size of that dependency problem grows, the benefit to the company grows exponentially, which is why MacOS and Windows are so dominant and their companies so rich. Maybe Apple should have gone under, on pure quality issues, long before Mac OS X, but the dependency of the design industry maybe kept them afloat until they could revitalize?

Iko, thanks for this reference. Not quite what I’m talking about, but very interesting at first glance.

J.Q.,

Here also is the link to the CasP site and all the Bichler/Nitzan archives.

https://capitalaspower.com/

I’ve recommended a couple of the papers from this site before but I will recommend them again in case you missed them.

“The Aggregation Problem: Implications for Ecological and Biophysical Economics” – Blair Fix.

“The Autocatalytic Sprawn of Pseudorational Mastery” – Ulf Martin.

These papers are crystal clear and quite superb in my opinion. The titles are probably the most opaque parts of them. All the necessary concepts are lucidly explained in the actual texts.

There’s a paper by Bichler and Nitzan which I want to find again too. I will post the link when I find it. It is directly related to the subject matter of your post, IIRC, and specifically compares capitalized market values to tangible book assets of GMH and Microsoft, again IIRC. B&N makes some interesting observations about the stark differences of the ratios.

See above. Oops “Sprawl” not “Sprawn”. My kingdom for a chance to amend my own posts.

Monopoly footnote on my hobby horse ARM. Currently it’s part of the sprawling Japanese Softbank investment conglomerate. Softbank made some bad bets elsewhere, and needs to raise cash, so it’s looking to sell the profitable ARM operation for $32bn or so. The midsized American electronics company Nvidia is actively seeking to buy. https://www.eetimes.com/nvidia-arm-deal-would-be-a-technology-disaster/

This is bad news. ARM is that rare creature, a benevolent monopolist. The monopoly is in the design of low-power computer processors or cores, which its licensees embed in SOCs (systems-on-a-chip) that go by the billions into electronic devices all the way from remote controls to smartphones and server racks. ARM has turned out benevolent by a conjunction of circumstances: it doesn’t manufacture anything and its sole revenue is from licensing core designs; its policy is to license to all comers without significant discrimination; the large ARM ecosystem provides substantial network benefits to the electronics industry, through standardisation of architecture and toolkits for design and testing; the licensing fees per core are kept low to discourage new entrants, including from among its own customers, some of which like Samsung and Apple are much larger than ARM; and it ploughs back a lot of its earnings into innovation, which again discourages new entrants, and stimulates downstream innovation by licensees. The Chinese government, often predatory on IP, is happy to let ARM collect its modest fees from many Chinese companies. See my conceit of ARM cores as mitochondria. https://www.samefacts.com/25-billion-turing-mitochondria/

ARM was OK as a small independent British company. It was OK as a pat of a hands-off Japanese investment conglomerate. It won’t be OK as part of an American electronics company that makes graphics cards, GPU designs and SOCs for self-driving cars, where it competes directly with other ARM licensees. The ecosystem could easily collapse. The second piece of bad news is that to prevent this gross policy failure, we are now reliant on the good sense of three governments: those of China, the USA, and the UK.

Do we really need tech monopoly horror to explain why stocks increase when real interest rates on bonds decrease? Expected future returns are adjusted that way. Suppose the implicit point here is that in a perfect market, one would just build competitors from scratch as long as the companies value is above replacment costs which can be aproximinated reasonably well with book value. But that is also not going to happen when A) companies were valued below replacment costs before the rise in valuations – which seems like a reasonable assumption for many, that number also should be at leat some above book value on average, even with ifrs/gaap goodwill accounting weirdness B) there is any kind of market power/barrier to entry far below tech monopoly level.

That list of companies according to R&D spending excludes Amazon by the way, which is overall by far the biggest r&d spender. Not that it matters to the point, its just a weird overseight.

“Do we really need tech monopoly horror to explain why stocks increase when real interest rates on bonds decrease?”

They are two sides of the same coin, as you say, I’m trying to explain the low rate of return on capital in general, and pointing out that equity markets aren’t a counterexample.

The low rate of return on equity? What am I missing? BHP now yields 5.8%, Commonwealth Bank 6%, Amcor 4.8% while listed investment companies like Argo and AFIC, which hold a broadly diversified portfolio of stocks, yield between 4 and 4.5%. In an era of close-to-zero inflation real yields seem high not low. Nor is it the Coronavirus that has temporarily driven yields up because of expectations of doom about the economy. The Dow is close to its peak having doubled since 2016 and the ASX is down less than 20% – not bad given the worst apparent economic collapse for a century and the rapid appreciation the ASX enjoyed in 2019. If anything investors seem overconfident.

Announcing the death of “capitalism” (I define as an economy where firms access their capital in private equity markets) seems premature.

This year, in Australia, there has been a crazy capital raising rush – more than $70b in the secondary market. Investors are attracted to the high real yields being offered and, despite fears about the future, are falling over themselves to gain access to equity claims.

https://www.afr.com/chanticleer/capital-raisings-could-crack-70b-20200429-p54o71

There is certainly something stranger than usual going on in “capitalism”. I would define capitalism as per the Wikipedia definition but with some caveats.

“Capitalism is an economic system based on the private ownership of the means of production and their operation for profit. Central characteristics of capitalism include private property and the recognition of property rights, capital accumulation, wage labor, voluntary exchange, a price system and competitive markets. – Wikipedia.

The one thing I would really cavil at in that definition is “competitive markets”. These rarely exist in pure form and tend to exist rather imperfectly in really existing capitalist economies. Of course, one has to add that really existing capitalist economies are not pure capitalist economies. They contain a necessary government control element to issue and manage fiat currency, to guarantee law and contracts and to back private property with policing, the justice system and other institutions. In mixed economies governments tend to provide welfare and social services and to run some nationalized entities.

However, given the above caveats, if the economy is more than 50% private (perhaps excluding self-employed and sole owner-proprietors not employing labor) and is as per the above caveat-ed Wikipedia definition then it could be described as essentially capitalist, especially as the private percentage rises higher.

Getting back to the strangeness. It is certainly strange to see share prices and returns on equity holding up on the stock markets at the same time as economies tank and real production crashes. There seems to be a disconnect there: fundamentals which are out of balance and which must come back into balance at some point. Cheap money (QE etc.) certainly plays a role in pumping up stock prices. It also permits greater allocations for dividends and other returns on equity. How long can this money stay in these circuits without leaking out to cause more than just asset inflation? I mean leaking out to cause goods and services inflation.

At the same time, rolling climate change induced disasters (bush-fires, hurricanes etc,) are destroying fixed capital at “unprecedented” rates and new fixed capital formation and general production are slowing down due to these effects and the coronavirus pandemic. This looks like a system to me that is highly out of balance, out of equilibrium, running down and suffering ever greater perturbations. In particular, the notional systems (money, paper assets, finances) seem badly out of whack with the real systems, meaning not only the real economy and real ecologies but also real people, their physiology and psychology.

The most volatile and rapidly reacting element(s), of the three real systems named, are real people; the “masses”. I expect masses of people, in the more disrupted countries at least, to go “ape-shit” [1] when they discover the real systems are not going to deliver them what they want and need. They will blame the political systems and finance systems for this and will be mostly right although of course mother nature (all natural laws) does actually “bat last” and hit hardest. The progressions could be: demonstrations, civil unrest, riots, rebellions, civil wars, regional wars, global war. There are possible circuit breakers to this progression. The biggest one overall would be full democratic socialism and eco-socialism with sustainable and circular-economy practices. Failing that, it’s a shit-show.

A trend that can’t continue won’t. – to rephrase Stein’s Law.

Note 1:

Ape-shit – A state of anger and rage that produces behavior more closely resembling that of an enraged ape than a human.

Shit-show – When everything turns out extremely horrible.

(Definitions edited from Urban Dictionary.)

“What am I missing? BHP now yields 5.8%, Commonwealth Bank 6%, Amcor 4.8%”

The first thing you might be missing is that those yields are not spectacular in a historical perspective. O good guesstimate of real historical equity return is about 6,5%. So if those yields keep growing with inflation, they still produce a real return below historical averages for the entire market. The other thing you might be missing is a reasonable expectation that those companies will yield less in the future than they have in the past? That is essentially it for most of the market isn´t it – the market as a whole is still a bit below peaks. However if something might have happened in the meantime that suggest significant worse returns, like maybe a pandemic, a bit below peak is still strange. This year is essentially a lost one – that is at least no positive return on assets, often worse for many companies and that is a loss that is supposed to be largely on the shoulders of equity, not debt investors. If is perfectly reasonable to expect decreases in stock values as a first aproximation even when a good covid outcome and no further secondary economic disruption are set as a 100% certain event

hix,

You are missing this. Share prices and returns on equity are holding up on the stock markets at the same time as real economies tank, real production crashes and lots of real people lose jobs. There is a disconnect. Stocks are out of balance with fundamentals and must come back into balance at some point.

Short answer? It’s time for a stock market and asset values crash. The market can stay irrational for a long time… sometimes. I am not sure a crisis of this magnitude is one where the stock market can stay irrational for a long period, even with Q.E. pumping and all the rest of it. Expect a crash at some point.

I can’t advice what investments to be in. I think fewer than 5% of stock market adepts and finance advisers would really know what to be in at the moment. I suspect they have and advocate complex and hedged positions for this current situation. Of course, if you don’t have much spare money then you don’t have this problem. Fully owning your own house on a bit of land (even a 1/4 acre) is handy. You are going to want separation from other people for a long time to come I think. If you don’t own a property yet, don’t rush. Wait for the (almost) inevitable property crash to make them cheaper. At least, that’s my guess.

My private investments are passive* and i would never pick individual stocks, at least not on any other criteria than geographic proximity and quality of the food at the annual meating. The allocation between asset classes is also passive. My investments are far to small to have a headache about anyway. Based on any conventional valuation metric local housing would be no better investment by the way. This is quite a different topic from the theory discussion. Fixed fee only advisors aren´t really a thing here and the provision salespeople tend to be far less competent than myself on bascical technical issues, They don´t know the first basics of portfolio theory or that such a thing as inflation index government bonds exists. I also never really understood the need to have financial advisors, even competent ones. They can´t magically do anything better than say a vanguard target retirment fund, at least not after costs. Note that both Australia and Germany are sort of oddities a bit on different ends of the spectrum regarding how people save in general and for retirment in particular as well as how that is regulated.

*(ok, this is not entirely true: Hope some obscure, still well regulated funds, kind of heritage products that will soon be a thing of the past are miscrpriced here, or at least an opportunity for a kind of tax rate arbitrage for poor people like me)

I agree that the entire privatized superannuation investment industry for average workers is a con. Workers would do better with a national superannuation scheme run by the national government, which the workers and government each pay into and which would give a defined percent of retirement income for retired life. Simple, effective, equitable and no need for private financial advisers taking fees. If people want to go beyond that AND have the extra income to go beyond that then they may join a private fund as well.

When I mistyped “private” just then, my spell checker was advising me “pirate”. It is one heck of a smart spell checker! 😉

James Wimberley – “The midsized American electronics company Nvidia”

Not quite midsized and more. Market cap exceeds Intel.

https://www.koyfin.com/share/3ZfaAhHiNr

Don´t you know, everyone is mid siced, at least in self description, no they are never ugly gigantic monopolies. Bosch also self describes as “mittelstand”. Here´s the thing however: Nvidia really is not exactly a giant based on revenue or employee numbers. Arguably, employees also get some small slice of the monopoly pie, or maybe they don´t and nvidia is just fakeing employee numbers massivly as many of those tech companies do by employing over 50% “contract workers”. Based on profit, things look already bigger, but even that one isn´t such a high number with a p/e of 85. What they are is an just about savely established quasi monopoly in some fast growing markets (machine learning /assits up to self driving cars. in addition to conventional graphic cards). I´m inclined to have a kind of maybe markets are not that efficient discount applied to such cases, not that it helps, still looks scary. Such companies just should not be for profits. If stock market prices have any basis in reality (and i tend to think yes) we are headed into an ugly world indeed.

Even the recent decline of Intel can be read in gloomy terms: Maybe intel is about to become an albeit unpredicted victim further semiconductor consolidation to ever bigger monopolies.At the end only tsm and samsung might be meaningfull chip manufacturers and development will be split 3-4 specialiced monopolies/duopolies.

On a wider front, Power = Monopoly. With reference to productivity gains compared to labor gains there seems to be an important inflection point (or rather inflection zone) from about 1972 to 1981. What happened at that time? Rather than looking for purely “economic causes” according to “economic laws” or even for causes exogenous to the political economy, I argue we should look for institutional causes via institutional changes.( Although, a full study looking at all potential causes would also be worthwhile.)

Economics (or political economy) is strongly institution-governed and institution-conditioned, in my opinion. The following would be my hypothesis. Institutional changes were made from that time to “discipline” labor and these changes were effective as designed. The monetarist and then neoliberal ideology had and has a bias and blind-spot which decrees that profits (including what critics might term excess profits) are not the cause or a contributing cause of inflation. Only wages, by instituted definition, could cause inflation in this view. The NAIRU (Non-Accelerating Inflation Rate of Unemployment) was theorized and then instituted in praxis (embodied in institutions and labor-industrial law). It referred to the theoretical level of unemployment below which inflation would be expected to rise. Unemployment was used to discipline wages. The high taxes which had been used to discipline excess and windfall profits were regressively abandoned.

A Non-Accelerating Inflation Rate of Profit was never theorized, at least not in conventional economics. Try searching for it. Yet why should it not be part of theory and praxis? Adam Smith did not simply argue that excess profits got competed away, though that is what his modern acolytes argue. As Adam Smith was well aware (being a moral philosopher and realist);

“People of the same trade seldom meet together, even for merriment and diversion, but the conversation ends in a conspiracy against the public, or in some contrivance to raise prices.”

Smith recognized the potential for what we can call guild or cartel behavior. Neoliberal apologists seek to reclaim this point from Smith as follows. “Smith’s point is that the only way businessmen can succeed in a ‘conspiracy against the public’ is if they are given protection by government regulation.” – Sam Bowman, Adam Smith Institute. To that I would say “A Daniel! Yea, A Daniel!” meaning (ironically in this case) that a wise judge has spoken . (See “The Merchant of Venice.”) If businessmen as a class, exploiting labor as a class, have succeeded in raising productivity by 246.6% since 1972 while only raising the hourly compensation of labor by 114.7%, then surely the key hypothesis following Adam Smith’s own reasoning, and that of his neoliberal acolytes, is that the businessmen indeed have been given protection and assistance by government regulation.

And that’s my hypothesis in a nutshell. Namely, that the institutional assistance (the favoring of a certain class) is the causative element in the change. In turn, as the cause of that cause, what political and power changes permitted and facilitated these institutional changes and the consequential class-differential assistance? That is the next and deeper question to be answered in modern political economy. The answers likely will be found in the inherent tendencies within capitalism itself. Marxist theory can come to our aid in this part of the analysis. The tendency to the oligopoly and monopoly accumulation of capital and the capturing of the propaganda arms (concentrated mass media) and governance arms (via representational and regulatory capture) of society will in turn, in all likelihood, explain the insitutional assistance changes.

Bourgeois or orthodox economics does not have natural laws which can be described mathematico-deductively. It is not a natural system with natural laws (like the climate system for example). It is a politically-generated social power system and prescribed formal system. It has not natural laws but legal laws and thence capitalist accounting and capitalization rules all backed by force (ultimately backed by the state’s monopoly of force, the monopoly of violence). Wherever an economic monopoly is found, a sociopolitical monopoly of force, meaning legal (or illegal), political, social and physical (kinetic) force will be found which underpins the monopoly and backs it. Nobody willingly accedes to a an immiserating, unjust dearth while others roll in ostentatious and happy plenty. The curtain of power is the differential osmotic membrane which permits violence to permeate mostly one way and rewards to permeate mostly the other way.

To quantitatively investigate the above assertion, the relative masses of such forces would need to be aggregated. How many security force personnel, batons, guns, bullets, rubber bullets and cylinders of tear gas are deployed on behalf of each side (capital and labor)? What and whom are they deployed to attack and what and whom are they deployed to protect? How many lawyers are deployed by and for each side? How many pages of legislation are deployed to protect the rights of capital and how many to protect the rights of labor? How much capital is deployed to fund pro-capitalist campaigns? How much is deployed to assist pro-labor campaigns?

The development of relatively objective metrics would be difficult but not impossible. Such studies would struggle even for funding. The extant system invests largely in creating, perpetuating and legitimating itself; certainly not in critically examining itself. That eximination has to come from outside the existing power systems and without compromising or treating with them. Compromise is accommodation. Accommodation is to be absorbed; catabolized and consumed by the system.

You say John that ‘Without these public goods, Google would be worthless.’ Not quite correctly phrased. Given the huge amount of information out there, an efficient search engine is immensely valuable. People would be willing to pay a huge amount for Google search if advertising didn’t pay for it. My understanding is that the Google boys were just interested in selling it as a search engine, and it was Eric Schmidt’s idea to attach advertising to it to pay for it. What I’m trying to say is that its the monoply nature of the search engine thats the key determinant of the value of Google, not whether part of its value comes from public goods or whether advertising pays for it. (Its an interesting side issue as to why advertising works to (at least partially) finance certain information products like free to air TV, newspapers and search engines but doesn’t work for other information products like books.

I dont think that houses will get cheaper if the stick market crashes. Real estate and Gold are refuges from the stock market. Slide at second base in to the sand pit?

Curt

Houses made of wood will get cheaper if the stick market crashes!

John Goss,

Not only that but then the capitalists will not be able to beat us with that stick by forcing us to buy in to the stick market to protect some sembalance of survival when we are old because the rulers routinely threaten to cut the benifits of the government retirement systems.

Just had the thought that in the middle ages we lived in a rentier economy with a small very small capitalist domain. So in a way we have gone full circle back to another monopoly based economy?

Just a thought.

[…] of Microsoft’s capital stock is less then 10 per cent of its market value. The rest is made up of intangibles, a polite word for monopoly-power network effects, intellectual property, and good old-fashioned […]