I wrote this for a Guardian panel. The published version was cut for space reasons, so here’s the full version

The central concern expressed by the Reserve Bank in defending its high-interest rate policy is that expectations of higher inflation may become entrenched, requiring a further, more painful round of contractionary monetary policy in the future. Even after stripping out the effects of various “cost of living measures”, the RBA’s estimated core inflation rate is only just above 3 per cent. This suggests extreme sensitivity to the risk of even a modest increase in the long run rate of inflation.

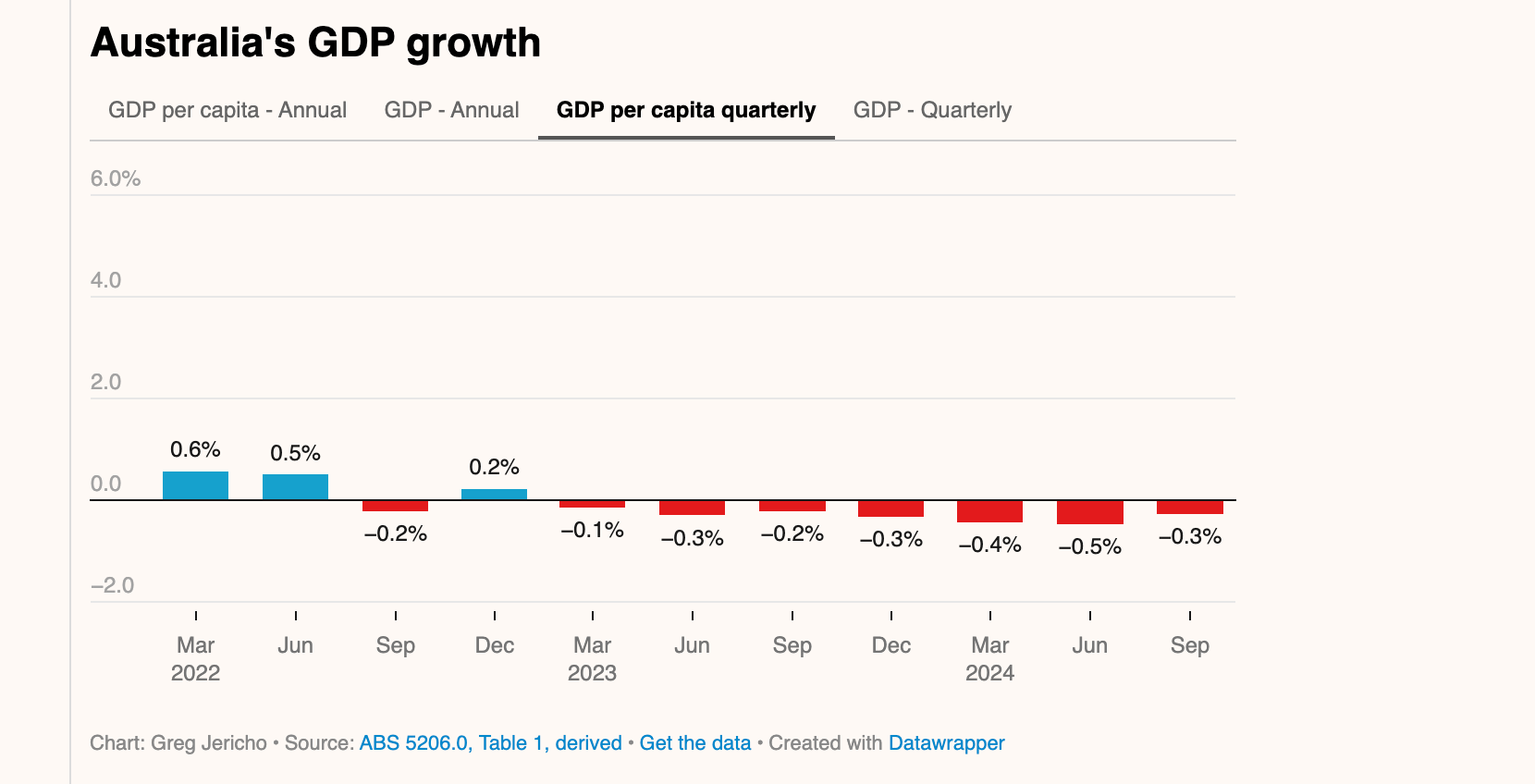

By contrast, the RBA expresses no concern that the reduction in economic growth induced by its policies will lead to a permanent reduction in living standards. The underlying assumption of the RBA’s macroeconomic model is that the economy will always return to a long-run growth path determined by technology and economic structure.

But there is ample evidence, notably from New Zealand and the UK to suggest that the loss in productive capacity associated with slowdowns and recessions is permanent or very close to it. Until the 1980s, the New Zealand and Australian economies grew almost in parallel. But from the early 1990s, onwards, while Australia has avoided recession (at least on the widely-used measure of two quarters of negative growth) for more than thirty years, New Zealand has had at least half a dozen. This miserable performance, reflecting both policy misjudgements and overzealous neoliberal reforms has resulted in New Zealand falling far behind Australia in terms of incomes and living standards. The steady flow of New Zealanders to our shores, and the lack of any comparable flow in the opposite direction, reflects this.

In the UK, the combined effects of the GFC, Conservative austerity policies and Brexit has produced a long period of stagnation in national income. As Brad DeLong observes, had Britain continued on its pre-2008 growth trend it would now be forty percent richer than it is today

The Unmaking of a Modern Economy: Brexit, Austerity, and Britain’s Great Retraction

Even though Australia has experienced a lengthy period of declining national income per person, the RBA does not even mention the risk of a permanent reduction in living standards. In its pursuit of rapid achievement of an essentially arbitrary inflation target, RBA monetary policy puts all our futures at risk

No. For each country cited, and similarly for some not, it’s the result of the ruling class neoliberals’ nation immiserating immigration ponzis. The RBA has no control over immigration numbers, no remit to set immigration nor population policies and targets, and no control of national nor state borders. The RBA has on occasion given a nod to their difficulties resulting from and obliquely mentioned the adverse impacts on the economy of ponzi immigration numbers. The Bank of Canada has by comparison blown a bullhorn on it.

When there is a complex wicked problem, people tend to fixate on one factor (often their favourite bête noire) as sole cause. We are dealing with a complex system with multifactor causality. Even more than that, we are dealing with a complex system which demonstrates emergent behaviours. While one populist approach might be to attribute inflation, across the board, to excess immigration another might be to attribute inflation to excess government spending. In both cases this is simplistic and misses the mark. I ought to note here that I am against the current rate of immigration into Australia which I do consider excessive on both environmental grounds and housing crisis grounds. I even agree it does play a strong role in some forms of inflation, like housing asset inflation. However, our real problem goes much deeper.

The real problem follows from the excess power of some blocs in our society. These blocs are essentially the oligarchs, the corporate elites and their allies, the political elites. These groups essentially have formed an alliance against the majority. We cannot, in the main, get policy for average people and poor people who together do form the great majority. In the main, we get policy which suits those above-mentioned power and wealth elites. Power and wealth have become entirely allied and fungible in our system.

The corollary of the excess power of some blocs is the inadequate power of other blocs. The main blocs who are weak in our system are firstly the great majority of the people. These are “the 99%”. While fractured, atomised and not acting in concert and with solidarity, the people are weak. Individually, we are weak against the forces of “capital as power” arrayed against us. The second important bloc which is also weak is small but potentially influential possessing a great deal of knowledge. Unfortunately some considerable proportion is faux knowledge, founded ontologically on its own normative assumptions. This group which is weak in power and influence in this system is the bloc of dissenting academics and intelligentsia. Currently, they too are weak and uninfluential.

Too many of the middle class, the upper middle class, the bourgeois merchants and trades (economically middle or upper middle and with materialist values and conventional attitudes) and the academics and intelligentsia have been co-opted to the current “capital as power” system in practice by the perquisites and comforts of their position. If we are honest, many of us will see we have been co-opted to the system in lived practice despite our professed enlightened concerns. It is almost impossible to swim against the current in practice so we swim in theory and opinion, myself included.

I do hold that those basically orthodox but still enlightened economists – who are concerned about fighting against climate change and the pandemic(s) era and are working in their way for equality, human rights and a healthy and sustainable people, society and economy – do not yet properly understand money, inflation and the phenomenon of “capital as power”.

They apparently do not understand the importance of empirical ontology. I do not speak here of metaphysical ontology which is a quite separate, speculative and unempirical subject. They talk and write of inflation, at least in short opinion pieces, as one simple unitary phenomenon. That is they talk and write as if they are saying there is one aggregate inflation rate which has adequate meaning for analytical, explanatory and policy purposes. This is plain wrong: empirically wrong and demonstrably so. Their position then entails entering the conventional argument and making their own arguments on those false grounds, on the false assumptions of orthodox and essentially capitalist economics. This is not, by the way, a Marxist argument, it’s a “Capital as Power” argument.

The path to take is to destroy, theoretically, the unempirical assumptions of classical and neoclassical economics as they pertain to money, finance, capital and their derivative phenomena like inflation. Of course, doing this would put one outside the tent, outside the entire echo chamber of conventional economics and indeed outside the “ecology” or “ecosystem” of professional economics.

To theoretically and logically destroy a raft of ideology (in this case the ideology of broadly conventional economics) and to put forward scientifically testable hypotheses would be to go against the whole establishment of conventional economics. Conventional economics is essentially a normative school not a descriptive or scientific school. Also, to take this tack would be to be misunderstood, ignored and shunned. It would also be to be uninfluential. But isn’t it the case that enlightened conventional economists are currently uninfluential anyway and perhaps have been so for at least the last half of their careers?

The current world will continue on its unenlightened course in any case. The anthropocene or “climatocene” will wax. The “pandemicene” will wax. Regional wars and regional collapses will wax. There is a lot of wax going on to the surface of our hollowing out system. We are all waxing up our shiny possessions and our shiny theories. But theory, even valid theory, is forceless while ideology and propaganda continue to grip the essentially bourgeois and petty-bourgeois collective, consumerist mind. The day the endless-growth and endless-wealth predictions fail and thus the day “prophecy fails”, the vast, shiny, brittle patina will crack and the monocoque system with no substantial internal supports will implode, all at once. If valid theory has been prepared, something might be salvaged. The task now is to prepare that new paradigm theory, not to keep waxing and shining the failed theories of the past.

I can write more about the empirical poverty and failure of the aggregate inflation concept and policies based on it, perhaps in a new sandpit. However, I doubt anyone will take any interest. I doubt anyone has read this far.

Do write more, Ikonoclast. “If you reach for a star, you might not get one. But you won’t come up with a handful of mud either.” …Capital as Power rings true but is a hefty subject even for the wider academy, it seems. Perhaps like Richard J Murphy, the youtuber you recently linked in another post (thanks), you may be able to distill and simplify the complexities for the lay person, and the time poor. Likewise, for “aggregate inflation”.

On inflation, the cost of east coast gas is another multiplying huge and increasingly adverse economic factor never mentioned by LibLab, rarely by the idiot media, nor by many others either on the take from, or out of fear of, or in support of the foreign gas cartel. The US has gas reserves on par with Australia, produces a similar volume, generates hefty foreign revenues that return to base from similar exported volumes, but has domestic reservation at dirt cheap prices that sees their economy booming and sees Australian manufacturing flocking there after having to shut down here. Here the cost of gas for thermal processes, or as electricity (spot gas sets the price for us all on the east coast. Albanese’s contractual limit doesn’t apply and is actually the floor price anyway), or as a chemical feedstock is insane. Albanese idiot future renewals policy wishes for and requires gas as a transition fuel for electricity generation, but no one is investing in such generation due to the cartel’s gouging price of gas. Dutton’s idiot future energy policy gets around the gouging cartel’s price of gas by sticking with coal. (Won’t someone ever stick it to the foreign gas cartel? Not likely.)

A note too that “housing asset inflation” though sorely multiplied by the immigration ponzi is not in the purview of the RBA. OTOH, also sorely exacerbated by the immigration ponzi, huge and increasingly unaffordable housing rent is.

Svante, I do think that the “Capital as Power” theorists and intellectual community (Jonathan Nitzan, Shimshon Bichler, Blair Fix, Ulf Martin et al) have come up with a scientific theory rather than an ideology. Their main writings are all available from their site. The texts I would initially recommend are:

1 – The Book “Capital as Power” (about 400 pages)

https://bnarchives.net/id/eprint/259/2/20090522_nb_casp_full_indexed.pdf

2 – The Essay “The Autocatalytic Sprawl of Pseudorational Mastery

https://bnarchives.net/id/eprint/606/2/20190500_martin_the_autocatalytic_sprawl_of_pseudorational_mastery_recasp.pdf

3 – The Essay “The Aggregation Problem: Implications for Ecological and Biophysical Economics”

https://bnarchives.net/id/eprint/577/2/20190100_fix_the_aggregation_problem_bpearq_preprint.pdf

You can search for more texts of interest at the Bichler and Nitzan archives.

Bichler and Nitzan et al. are the only theorists I am aware of who have effectively demonstrated that conventional economics theories (classical, neoclassical and Marxist) are not fundamentally scientific theories. The main problem is that the fundamental ontology is flawed. (A little more on that later perhaps.)

The main operative problem is the “real-nominal bifurcation”. This can be précised as follows.

“Performing the Real-Nominal Bifurcation” May 11, 2015

DT Cochrane

The Globe & Mail recently published a roundup of seven analysis of the Canadian housing sector. All of the analyses took some position on whether or not housing in Canada is “overvalued.” The positions ranged from 60 percent overvalued to seven percent under-valued. Regardless of the position, all of the analyses – at least as presented in the roundup – have a built in presumption that nominal housing prices deviate from the ‘real’ value of houses.

This constitutes what some social theorists call a “performance” of the real-nominal bifurcation: (which bifurcation) Nitzan and Bichler argue is one of the foundations of (orthodox and even Marxist) political economy. The performativity thesis is perhaps most associated with Judith Butler, who argues that gender norms are continually reconstituted and reinforced by gendered activity. Several theorists have taken the idea of performativity into the worlds of economics and finance, most notably in “Do Economists Make Markets? : On the Performativity of Economics” – Donald A. MacKenzie, Fabian Muniesa, Lucia Siu. These theorists suggest that through theorizing, policy making, algorithm designing, accounting, advising, trading and other activities, economists and others in the world of finance perform functions that generate, and regenerate, the very markets of which they are supposedly objective observers.

For the analysts of Canadian housing prices, the basis for their claims of over- or under-valuation is eminently practical. They are assessing people’s ability to continue to afford homes at current price levels. As such, they compare housing prices to other quantities like income and bond rates in making their calculations. However, these analyses must be placed in relation to other economic discourses and analytical practices, such as the calculation of ‘real GDP,’ that normalize the price-value distinction. ‘Real GDP’ is similarly intended to serve a practical purpose. It is meant to allow year-to-year comparison of an economy’s performance by conveying the value of goods and services produced, after the effects of price changes are removed. The problem is in the ontological basis of this claim, which is that nominal prices are – at best – a distorted representation of the underlying real value. This then leads to a fundamental misunderstanding of what financial quantities are and what they do.

The practical intent of the over/under-valuation thesis is somewhat different in that it attempts to locate current prices in relation to future prices, which are expected to revert toward the true value of the homes. Those values are supposedly ‘revealed’ through the analysis of other metrics, such as income. Like with real vs. nominal GDP, the actual quantities – the ones we can observe – are deemed to be a distorted representation, failing to properly reveal the real value.

The economists who perform these analyses likely give little, if any, consideration to the ontological foundations of their concepts. If they’ve even heard of value debates, they probably consider it a passé relic from the history of economic thought. However, far from having been left behind, uncritical use of economic concepts entrenches, and naturalizes, a particular conception of value. It is in this way that the real-nominal bifurcation gets reconstituted and reinforced. Although, as Nitzan and Bichler argue, there is no real value that nominal values imperfectly represent, the bifurcation itself is very real, made so by the very performances it facilitates.”

That’s enough for now. What are the chances that Capital as Power will ever be taken seriously in the mainstream? Probably very low. It is complicated and the endlessly repeated “for-public-consumption” myths of market economics are simple ideological slogans by comparison and are taken on faith by the brain-washed, product-washed population. Reality always is complicated of course and particularly so when the physis (nature) and the nomos (law and custom) interact. Nobody understands reality. A few perhaps can gain a glimpse of slivers of it. The majority prefer to live in sensations, dreams, wishes and magical beliefs when the nomos can provide them and cushion harsh reality. We have actually evolved that way (biologically and culturally) to a very considerable extent to cement eusociality and the survival value it has conferred to our species, so it is not fair or kind, ultimately, to fling blame or contempt. We humans can scarcely help ourselves.

However, what are the chances that this system of capitalism, consumption and bifurcated reality is sustainable? Those chances are very close to zero now on any scientific analysis. What I am saying is that we are highly unlikely to argue away this doomed system. The processes of the physis will refute the unfit nomos. It has become as stark as that. The best we can do now is understand the collapse and the reasons behind it, view it philosophically and prepare new and scientifically valid theory for a remnant who may be able to use it and save something and some of themselves, I mean relative to the 8 billion alive currently. Perhaps a couple of hundred million humans could be alive in a couple of centuries time. If they keep the knowledge, understanding and the visceral and agonising feel of what happened they might be rather wiser compared to us. They will certainly know a lot of political economy constructions to avoid, if they can retain the key histories, libraries and databases.